This standard document is developed to offer you the best possible overview of the conditions of the home loan credit on offer. The ESIS supplies the following info: the of the loan the of the loan the type of the total amount to be repaid the (APRC): a single figure representing the total expense of the loan, expressed as a yearly portion.

If you have not gotten the ESIS kind from your lender, you can request it. Under EU rules, the lender or credit intermediary needs to give you; some EU countries' nationwide law will give you more time. how do balloon mortgages work. Depending upon the country where you are making an application for your loan, this could either be: a, throughout which you can think about whether the deal fits you a duration during which you can from the credit arrangement you have actually already signed a combination of the 2.

This enables you to stop paying interest on outstanding financial obligation, or transfer to a more beneficial home mortgage offer, including from a various lending institution. National guidelines figure out in this case whether the lender can ask you to pay if you terminate your home mortgage loan earlier than predicted. Where suitable, such settlement should never ever go beyond the financial loss of the lender.

All about How Do Reverse Mortgages Really Work?

They might propose a policy to you in a bundle with your home loan credit contract; however this can not be made a condition for you to acquire the home mortgage credit. You are from other insurance companies, as long as the level of guarantee provided by various policies is equivalent to what is required by the lending institution.

Buying a house is an experience. First you find out how much house you can manage. Later on comes the home mortgage. Understanding how to get the finest home loan rate begins with knowing the responses to these six questions: Home mortgages have actually either repaired rates of interest or adjustable rates. Fixed-rate home loans lock you into a constant interest rate that you'll pay over the life of the loan.

The interest rate on an adjustable-rate home mortgage can alter over time. An ARM usually begins with an introductory period of 10, 7, 5 or 3 years (or perhaps one year), during which your rates of interest holds stable. After that, the rate might change regularly. ARMs normally provide lower initial rates.

Rumored Buzz on What Work Is Mortgages?

One point is 1% of the loan quantity, which normally reduces the mortgage Click here to find out more rate by 0. 25%, although the reduction can vary. If you take out a loan at 4. 5% interest, you might be able to pay a $2,000 charge to lower the rate to 4. 25%. When you pay discount points, you normally shell out thousands of dollars in advance to conserve a few dollars monthly.

This break-even duration differs depending on loan quantity, the cost of the points and the rates of interest. It's typically 7 to nine years. If you do not prepare to have the loan for that long, it's a great concept to avoid the discount points.Closing costs are fees charged by the lending institution and 3rd parties. But they do have an influence on your wallet. Closing expenses usually amount to about 3% of the purchase price of your house and are paid at the time lauren jenifer gates you close, or complete, the purchase. Closing costs make up different fees, consisting of the lender's underwriting and processing charges, and title insurance and appraisal charges, among others. Prior to you settle on a home loan.

, learn if you're qualified for any special programs that make homebuying less expensive. Lots of states offer aid to first-time house purchasers in addition to repeat buyers. Each state offers its own mix of programs for home purchasers. Lots of states provide down payment support, often combined with favorable interest rates and tax breaks. Get responses to questions about your mortgage, travel, finances and preserving.

How How Mortgages Work For Dummies can Save You Time, Stress, and Money.

your assurance. Veterans and rural debtors might receive loans that allow 100% funding, requiring no down payment. Other borrowers might get approved for home loans that enable down payments as small as 3% or 3. 5%. Here's a summary: VA loans: If you( or your partner )are active military or a veteran,you mightget approved for a home loan guaranteed by the Department of Veterans Affairs.USDA loans: If you live in a rural location, the Department of Agriculture might guarantee a low- or no-down-payment home mortgage and assistance https://zenwriting.net/sindurj3jw/with-a-traditional-home-loan-you-obtain-money-in-advance-and-pay-the-loan-down cover closing costs.FHA loans: Home loans insured by the Federal Housing Administration enable deposits as low as 3.FHA-insured loans are more flexible of low credit report, but you pay for home mortgage insurance for the life of the loan.Conventional loans.

with 3% down: Some customers may get approved for traditional loans, which aren't guaranteed by the government, that allow down payments as low as 3%. The home loans typically are fornovice or low- to moderate-income borrowers. Here are suggestions for comparing loan deals: Buy loans within a set window of time. The 3 big credit bureaus motivate you to search.

You have 14 to 45 days, depending on the scoring design, to get as lots of home loans as you desire with the very same effect on your credit report as obtaining one loan. Each lending institution is required to offer a Loan Quote form with information of each loan's terms and charges. The Loan Quote is designed to simplify the task of comparing home loan deals. ONE Home Loan is a 30-year fixed rate loan with a 3 percent down-payment and some of the most affordable rates of interest around. With ONE Home mortgage, you will never ever have to pay for personal mortgage insurance coverage.

The Ultimate Guide To How Do Interest Only Mortgages Work

( PMI ), saving you numerous dollars on a monthly basis. In addition, qualified debtors will get an additional aid to decrease their month-to-month payments. Over 40 lenders around the Commonwealth deal ONE Mortgage. To learn more and to use our calculator to see what you can pay for, go to https://www. mhp.net/one-mortgage. The ONE Mortgage has four features that make buying a.

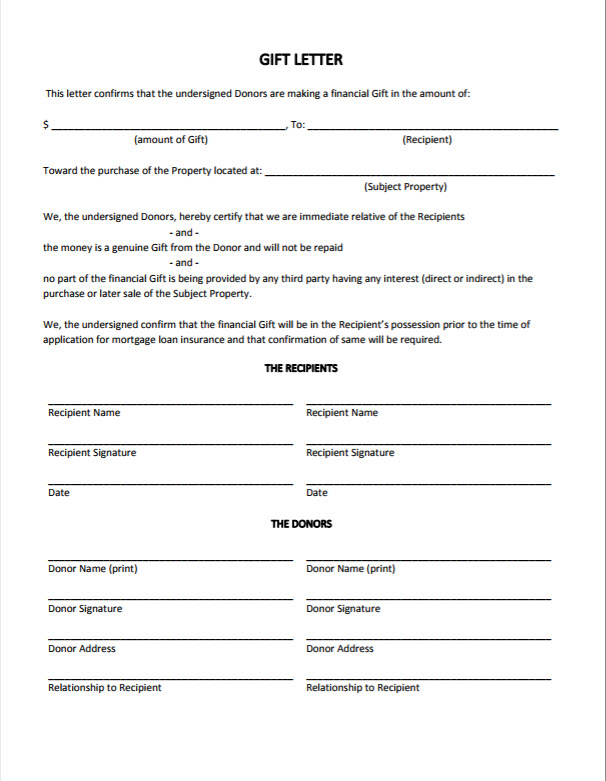

home really budget-friendly: 3 percent minimum down-payment Low fixed rate of interest No Private Mortgage Insurance Coverage( PMI) Additional help that decreases your regular monthly payments With these functions, ONE Home mortgage can decrease your monthly payments by hundreds of dollars every month compared to other 30-year home loans. To get a ONE Mortgage, you must: Be a newbie property buyer. This indicates that you have not owned a house at any point in the last 3 years. Take a property buyer class. This class will assist you prepare yourself for the home-buying procedure. Meet our down payment requirements. We need a 3 percent deposit to buy a condominium, single-family home, or two-family home. You may use a deposit program or gifted cash from a family member as part of this deposit. Have a total home income under our limits. These earnings restricts differ by neighborhood and the variety of individuals in your household. Have less than $75,000 in overall home possessions. But it does not include most retirement and college savings accounts. Meet our credit rating limits. Your credit rating should be at least 640 to purchase a single household or apartment and a minimum of 660 to purchase a two/three household house. We likewise have choices for people who don't have any credit rating.